I’m a financial advisor by trade but when I’m not working I’m spending a lot of time contemplating about life because life really fascinates me! It’s one of those things that you will never know what is really about because it changes constantly as you evolve every second. What life means to you may not mean the same to others. Since no one has THE answer about the meaning of life it becomes how we perceive life individually. In other words, we live in a reality that we have created entirely based on our own unique perceptions of what life should be at the moment. Therefore, at this very moment, life to me is like this…

For over 20 years being a financial advisor I never really put the two together until recently it came to me as another profound realization of life. It happened to be on a day that I didn’t feel well mentally. While I was reflecting on how crappy I felt at that moment something just clicked! I realized how many of these crappy moments I had felt in the past years of my life. I don’t track these moments but if I have to guess I’d say probably in the thousands! Now, I’m not saying I had a very terrible day that I felt depressed. It was one of those days that I just didn’t feel very positive. A series of negative thoughts arose all of the sudden for no reason, however, for the most part, I must say I’m a very positive person and I am well aware this is normal.

Anyway, I realized that after thousands of these moments I still managed to survive and became the person I am happy to be today. I asked myself if I’d go back in time to change all those little crappy moments. My answer was a firm NO! Not only would I not get rid of those moments in my life, I also wouldn’t erase the darkest period of times that I went through to get here. Why? Because without them I wouldn’t be exactly who I am today. When I say “them” I mean every part of my being, every difficult situation I went through, every person I met, every trouble I got into, every “F” I scored from my exams, every mistake I made, every cold I had, every bruise I got, every tear I dropped, every pain I endured, every negative or positive thought I had, every emotion I felt, every moment of loneliness and fear I experienced, etc. You get the point. To reject any of them is to be ungrateful of my past, or the life lessons I had been given, and not accepting or being unsatisfied with who and where I am today. There are still many things I need to work on but that doesn’t mean I’m not satisfied with what I have accomplished so far. As long as I’m aware that my personal development is a lifelong process and I have things to work on I know I’m on the right track. Believing I can only get better from here is what keeps me going! With this mindset I will not be ungrateful of whatever the universe presents to me and I know happiness is just within arms reach.

Let me demonstrate this logic with the Dow Jones Industrial Average historical chart since this is what I’m familiar with. Believe or not the two resemble each other awfully a lot.

Let’s call this chart the Dow Jones Individual Average and let’s pretend this is your life as Dow Jones.

For over 20 years being a financial advisor I never really put the two together until recently it came to me as another profound realization of life. It happened to be on a day that I didn’t feel well mentally. While I was reflecting on how crappy I felt at that moment something just clicked! I realized how many of these crappy moments I had felt in the past years of my life. I don’t track these moments but if I have to guess I’d say probably in the thousands! Now, I’m not saying I had a very terrible day that I felt depressed. It was one of those days that I just didn’t feel very positive. A series of negative thoughts arose all of the sudden for no reason, however, for the most part, I must say I’m a very positive person and I am well aware this is normal.

Anyway, I realized that after thousands of these moments I still managed to survive and became the person I am happy to be today. I asked myself if I’d go back in time to change all those little crappy moments. My answer was a firm NO! Not only would I not get rid of those moments in my life, I also wouldn’t erase the darkest period of times that I went through to get here. Why? Because without them I wouldn’t be exactly who I am today. When I say “them” I mean every part of my being, every difficult situation I went through, every person I met, every trouble I got into, every “F” I scored from my exams, every mistake I made, every cold I had, every bruise I got, every tear I dropped, every pain I endured, every negative or positive thought I had, every emotion I felt, every moment of loneliness and fear I experienced, etc. You get the point. To reject any of them is to be ungrateful of my past, or the life lessons I had been given, and not accepting or being unsatisfied with who and where I am today. There are still many things I need to work on but that doesn’t mean I’m not satisfied with what I have accomplished so far. As long as I’m aware that my personal development is a lifelong process and I have things to work on I know I’m on the right track. Believing I can only get better from here is what keeps me going! With this mindset I will not be ungrateful of whatever the universe presents to me and I know happiness is just within arms reach.

Let me demonstrate this logic with the Dow Jones Industrial Average historical chart since this is what I’m familiar with. Believe or not the two resemble each other awfully a lot.

Let’s call this chart the Dow Jones Individual Average and let’s pretend this is your life as Dow Jones.

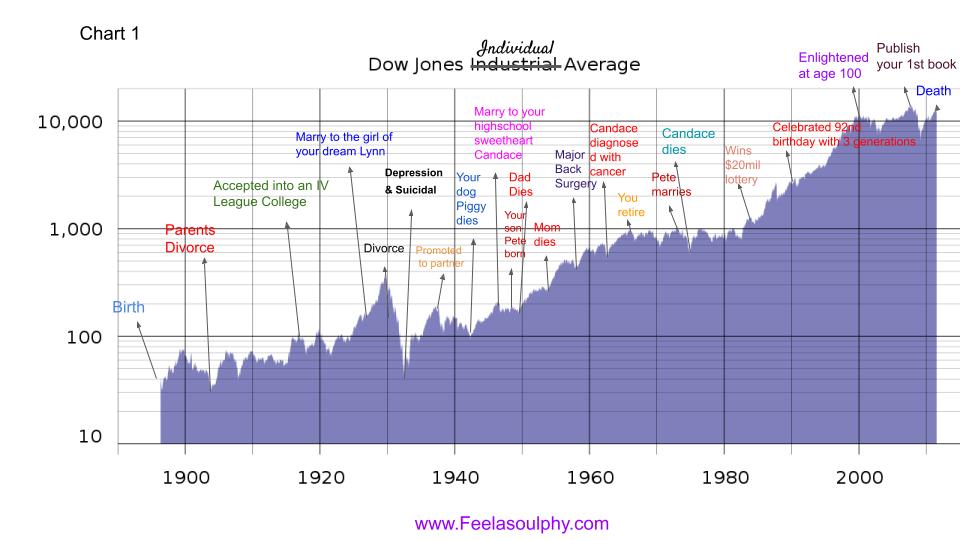

Chart 1 illustrates your lifespan from the day you were born to the day you passed away. I know this might look too good to be true because our average lifespan is not that long but this was the best chart I could find so we’re going to have to work with what I got! (Full disclosure: I’m not a good chart maker.) This seems like a pretty typical life in America if you ask me. It’s a good life but it’s nothing extraordinary or extremely dramatic. You might argue that this is not typical or this is too good of a life or this is okay or whatever, but I’ll ask for your patience until the end of the demonstration so you will see my point.

I believe this chart is self-explanatory so I’m not going into each event that’s marked on the chart. To summarize this chart, I’ll say life is unpredictable and it has its ups and downs. Some days you are on the top of the world and other days you are in the deepest ditch that you feel like you will never climb out of! However, life somehow finds its way to go on and finishes strong!

Let’s take a closer look at one event to understand better what I’m showing you. You see that big dip around 1930? You seem to be experiencing some kind of melt-down during that time after your divorce with Lynn. You were even suicidal. It took you a while to get out of that dip. I’m glad you didn’t pull the trigger or else you wouldn’t have had such a beautiful life later and given even more beautiful lives to so many of your offspring for generations to come. Your decision to continue living was a good one to say the least.

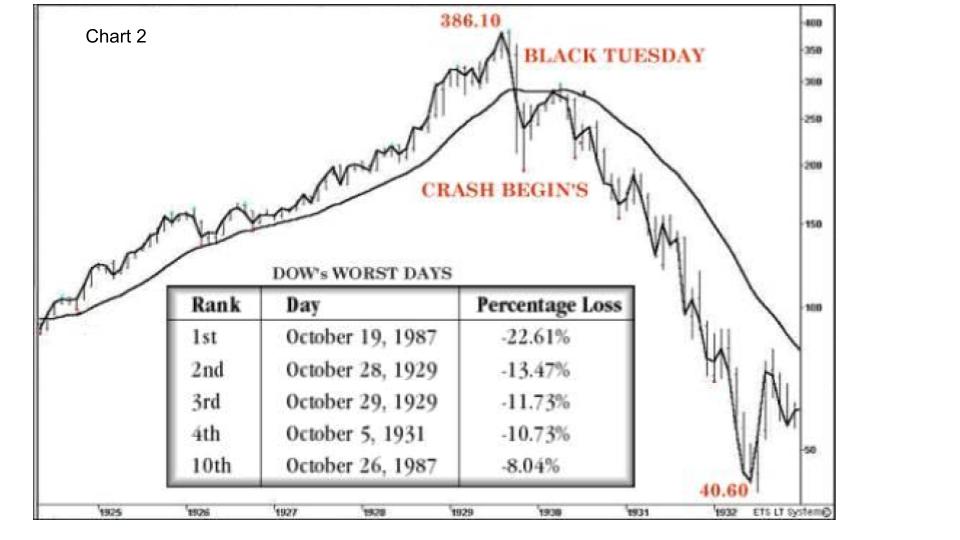

If you didn’t know, this is The Great Depression that happened in the history of the US. Just in a couple of years, DJIA dropped from 386.10 to 40.60. That’s almost a 90% decline! If you invested $100k to begin with now you only have $10k left! Ouch!

I believe this chart is self-explanatory so I’m not going into each event that’s marked on the chart. To summarize this chart, I’ll say life is unpredictable and it has its ups and downs. Some days you are on the top of the world and other days you are in the deepest ditch that you feel like you will never climb out of! However, life somehow finds its way to go on and finishes strong!

Let’s take a closer look at one event to understand better what I’m showing you. You see that big dip around 1930? You seem to be experiencing some kind of melt-down during that time after your divorce with Lynn. You were even suicidal. It took you a while to get out of that dip. I’m glad you didn’t pull the trigger or else you wouldn’t have had such a beautiful life later and given even more beautiful lives to so many of your offspring for generations to come. Your decision to continue living was a good one to say the least.

If you didn’t know, this is The Great Depression that happened in the history of the US. Just in a couple of years, DJIA dropped from 386.10 to 40.60. That’s almost a 90% decline! If you invested $100k to begin with now you only have $10k left! Ouch!

Zooming into the chart, here you can see why you were suicidal. You experienced a mental breakdown and watched your life freefalling! I can only imagine what you went through during that time. Nevertheless, good for you that you didn’t fold. You didn’t give up. You didn’t realize your losses.

In finance, we believe that money invested in the stock market is just paper money that has no real value until the profit or loss is realized, meaning to sell your positions. Once sold, you will be able to collect the proceeds or materialize your losses. At that time, everything is finalized with that particular transaction. If you made a profit you will be able to keep your profit for good if you never invest it again. However, if you lose money you will not gain your money back unless you go back into the market and even if you do there’s no guarantee you will gain it all back. I have seen this many times in my short 21 year career that people exit at the wrong time and they never had another chance to make it back in for a while because the market rebounded too quickly. Last year’s COVID correction was a good example. Even if you do make back what you lost long after you have already missed the opportunity to make more because you missed the beginning part of the recovery. For the younger folks this type of loss may still be tolerable but for the ones that are approaching retirement or already in retirement it can be catastrophic. They may never make the money back due to lack of time. You can see in chart 3 below, it took the market almost 30 years to get back to its original point in the 1930's.

If you committed suicide that would have been the end of your life where you would not have had another opportunity to recover from this and learned from your mistakes to improve your life for the better. You’d have lost forever!

Talking about bad days, there have been some really terrible ones in the life of Dow’s. You can see from chart 2 that the worst one yet was on 10/19/1987. In one day, it dropped 22.61%! I don’t know about you, even for a financial professional like myself would have felt like the end of the world is approaching! But that too shall pass and it certainly has!

Although when you are in the middle of the drop it can feel like it’s never going to end if you can hold onto this wild ride for just a little longer you will see the light at the end of the tunnel. See chart 3. In this chart, I want to show you why you should always hang on tight and you will always get through the tough times. There’s no drop that is too big for you to rebound in life unless life ends!

It’s worth mentioning that in investing, there are times that you have to strategically “quiet” or take your losses due to opportunity cost, this means you can potentially benefit more if you use your time and resources somewhere else. We can tactically manage the accounts where we are free to go in and out of the market as we wish to seek opportunities to maximize profits or minimize risks. That would be part of capitalizing the opportunities during market volatilities. We also don’t need to wait for 30 years for the market to rebound completely! Without these drops it’ll be hard for us to get into the market with new money. We are always looking for these opportunities to enter, re-enter, and exit the market temporarily. Of course, the gain is never guaranteed, but what is guaranteed is the learning experiences which can potentially help us succeed in the future. This is how all portfolio managers learned to manage portfolios. However, in order to do this it requires us to stay in the game without being completely checked out forever. This is also similar to poker games in which your goal is to last as long as your last opponent so you have a chance to see the opportunities presented to you to make a comeback.

Here’s a formula for you if you want to succeed at whatever you want to accomplish in life. It's a simple one and anyone can do it. Chances are you are already doing it without awareness so this formula will give you a nice clean visual to help you comprehend this process better. I believe it’s one thing to be successful and another to understand and remember how you became successful. If you have a formula to success you can duplicate the formula for anything you do.

In finance, we believe that money invested in the stock market is just paper money that has no real value until the profit or loss is realized, meaning to sell your positions. Once sold, you will be able to collect the proceeds or materialize your losses. At that time, everything is finalized with that particular transaction. If you made a profit you will be able to keep your profit for good if you never invest it again. However, if you lose money you will not gain your money back unless you go back into the market and even if you do there’s no guarantee you will gain it all back. I have seen this many times in my short 21 year career that people exit at the wrong time and they never had another chance to make it back in for a while because the market rebounded too quickly. Last year’s COVID correction was a good example. Even if you do make back what you lost long after you have already missed the opportunity to make more because you missed the beginning part of the recovery. For the younger folks this type of loss may still be tolerable but for the ones that are approaching retirement or already in retirement it can be catastrophic. They may never make the money back due to lack of time. You can see in chart 3 below, it took the market almost 30 years to get back to its original point in the 1930's.

If you committed suicide that would have been the end of your life where you would not have had another opportunity to recover from this and learned from your mistakes to improve your life for the better. You’d have lost forever!

Talking about bad days, there have been some really terrible ones in the life of Dow’s. You can see from chart 2 that the worst one yet was on 10/19/1987. In one day, it dropped 22.61%! I don’t know about you, even for a financial professional like myself would have felt like the end of the world is approaching! But that too shall pass and it certainly has!

Although when you are in the middle of the drop it can feel like it’s never going to end if you can hold onto this wild ride for just a little longer you will see the light at the end of the tunnel. See chart 3. In this chart, I want to show you why you should always hang on tight and you will always get through the tough times. There’s no drop that is too big for you to rebound in life unless life ends!

It’s worth mentioning that in investing, there are times that you have to strategically “quiet” or take your losses due to opportunity cost, this means you can potentially benefit more if you use your time and resources somewhere else. We can tactically manage the accounts where we are free to go in and out of the market as we wish to seek opportunities to maximize profits or minimize risks. That would be part of capitalizing the opportunities during market volatilities. We also don’t need to wait for 30 years for the market to rebound completely! Without these drops it’ll be hard for us to get into the market with new money. We are always looking for these opportunities to enter, re-enter, and exit the market temporarily. Of course, the gain is never guaranteed, but what is guaranteed is the learning experiences which can potentially help us succeed in the future. This is how all portfolio managers learned to manage portfolios. However, in order to do this it requires us to stay in the game without being completely checked out forever. This is also similar to poker games in which your goal is to last as long as your last opponent so you have a chance to see the opportunities presented to you to make a comeback.

Here’s a formula for you if you want to succeed at whatever you want to accomplish in life. It's a simple one and anyone can do it. Chances are you are already doing it without awareness so this formula will give you a nice clean visual to help you comprehend this process better. I believe it’s one thing to be successful and another to understand and remember how you became successful. If you have a formula to success you can duplicate the formula for anything you do.

Risks + Failures + Time = Experiences + Opportunities = Success

Risks: Anything you want to do that makes you feel fearful or uncomfortable because it could cost you something you value.

Failures: Anything you tried to do but not able to achieve your desired outcome.

Time: Anything + Time will create changes. Time = Patience. If you don’t have patience you don’t have time on your side. You will last as long as your patience lasts you.

Experiences: This is acquired from the total of the first part of the equation.

Opportunities: Without the first 4 this is hard to come by and even when they are presented to you you wouldn’t recognize what they look like.

Success: This doesn’t have to be the ultimate success you are trying to achieve. You can see on the chart where I have placed it in multiple points. In reality, they are everywhere, but because they are not THE success we are trying to reach they are often overlooked. Every success involves the first 5 elements including the big one you are shooting for but don’t forget to celebrate the small ones because they are building you up to the big one! If you understand how you have achieved every little success you will eventually figure out how to get to your final goal.

To summarize my findings, I realized that my moment of crappiness was very temporary just like all the other thousands of them I had before. It took me 1 min to get out of that one crappy mood by realizing how great and important the other crappy moments were. All of them together summed up the person I am today. For that reason, I wouldn’t trade them in for anything! Furthermore, I realized that had I not been working on myself for the past years to become a more positive person it might have taken me a lot longer to get over that crappy feeling. With this elevated self-awareness I was able to see it from a slightly different angle even maybe as small as by taking one tiny step to the left. This proves how critical self-development is. Thus, I believe the only project we are working on in life is ourselves and no one else.

Your life is based on how you perceive it. The more angles you see the better chance you will not get stuck in life for long. You will be able to quickly maneuver out of certain situations and free yourself from the long lasting agony. Sometimes, you can be one thought away from becoming depressed or getting out of depression. The ability to perceive in a multidimensional way is a valuable life tool to get unstuck so you will walk further in life to see that light at the end of the tunnel. Remember, all you have to do is to hang on tight and give it time and patience. So long as you are still in the game you will have the opportunities to get better and even succeed in life. Everyone experiences the ups and downs and there’s no way to avoid the downs. However, if you can find the opportunities in the midst of chaos you will be able to get back into the market and stay in the game! The more experiences you gain the better chances you will succeed in the future. That’s why I put “Experiences” in the 3rd chart to show you that the graph is not representing wealth accumulation but life experiences. With these valuable experiences you can take on the toughest challenges in life and ensure your life will be continuing on an upward trajectory like the DJIA.

Additionally, this is the same for relationships and marriages. Oftentimes we are tempted to walk out of our relationships because that’s the easiest thing to do - to not deal with it. In the end, we find ourselves continuing to face the same issues, just with different people in different situations. Sometimes, all we need is more time and patience and the willingness to work on ourselves instead of our partner to get over that hump.

Lastly, I’d like to end this by saying that we have the power to create our own life chart. There’s not one way to draw it because it’s fully customizable to our individual desires! Regardless how it has turned out so far there’s always a chance to make positive changes as long as we are still here. Let’s go out there and paint the most beautiful chart of our life!

Risks: Anything you want to do that makes you feel fearful or uncomfortable because it could cost you something you value.

Failures: Anything you tried to do but not able to achieve your desired outcome.

Time: Anything + Time will create changes. Time = Patience. If you don’t have patience you don’t have time on your side. You will last as long as your patience lasts you.

Experiences: This is acquired from the total of the first part of the equation.

Opportunities: Without the first 4 this is hard to come by and even when they are presented to you you wouldn’t recognize what they look like.

Success: This doesn’t have to be the ultimate success you are trying to achieve. You can see on the chart where I have placed it in multiple points. In reality, they are everywhere, but because they are not THE success we are trying to reach they are often overlooked. Every success involves the first 5 elements including the big one you are shooting for but don’t forget to celebrate the small ones because they are building you up to the big one! If you understand how you have achieved every little success you will eventually figure out how to get to your final goal.

To summarize my findings, I realized that my moment of crappiness was very temporary just like all the other thousands of them I had before. It took me 1 min to get out of that one crappy mood by realizing how great and important the other crappy moments were. All of them together summed up the person I am today. For that reason, I wouldn’t trade them in for anything! Furthermore, I realized that had I not been working on myself for the past years to become a more positive person it might have taken me a lot longer to get over that crappy feeling. With this elevated self-awareness I was able to see it from a slightly different angle even maybe as small as by taking one tiny step to the left. This proves how critical self-development is. Thus, I believe the only project we are working on in life is ourselves and no one else.

Your life is based on how you perceive it. The more angles you see the better chance you will not get stuck in life for long. You will be able to quickly maneuver out of certain situations and free yourself from the long lasting agony. Sometimes, you can be one thought away from becoming depressed or getting out of depression. The ability to perceive in a multidimensional way is a valuable life tool to get unstuck so you will walk further in life to see that light at the end of the tunnel. Remember, all you have to do is to hang on tight and give it time and patience. So long as you are still in the game you will have the opportunities to get better and even succeed in life. Everyone experiences the ups and downs and there’s no way to avoid the downs. However, if you can find the opportunities in the midst of chaos you will be able to get back into the market and stay in the game! The more experiences you gain the better chances you will succeed in the future. That’s why I put “Experiences” in the 3rd chart to show you that the graph is not representing wealth accumulation but life experiences. With these valuable experiences you can take on the toughest challenges in life and ensure your life will be continuing on an upward trajectory like the DJIA.

Additionally, this is the same for relationships and marriages. Oftentimes we are tempted to walk out of our relationships because that’s the easiest thing to do - to not deal with it. In the end, we find ourselves continuing to face the same issues, just with different people in different situations. Sometimes, all we need is more time and patience and the willingness to work on ourselves instead of our partner to get over that hump.

Lastly, I’d like to end this by saying that we have the power to create our own life chart. There’s not one way to draw it because it’s fully customizable to our individual desires! Regardless how it has turned out so far there’s always a chance to make positive changes as long as we are still here. Let’s go out there and paint the most beautiful chart of our life!

RSS Feed

RSS Feed